Tax-Advantaged Education Accounts - Why You Should Contribute

AdviceBy_ #8

In my previous article, we discussed 401(k)s. Today, we’ll discuss Education Accounts. Education, notably higher education, is costly. The accounts we’ll discuss can help you pay for educational expenses (college, graduate school, K-12) with money that’s not taxed. Share this with your friends and subscribe above to get the following articles on Credit Cards straight to your inbox! Disclaimer: nothing here is financial advice, just my personal thoughts/learnings.

Part 1: Savings vs. Checkings Account (read here)

Part 2.1: Investing - Definitions (read here)

Part 2.2: Investing - Start Now (read here)

Part 3.1: Retirement Accounts - Roth IRA (read here)

Part 3.2: Retirement Accounts - 401(k) (read here)

Part 3.3: Education Accounts - 529 & Coverdell (this one!!)

Part 4: Credit Cards

📝 Today’s Agenda (529 Plan & Coverdell)

Why Are Tax-Advantaged Accounts Important? • What are Tax-Advantaged Education Accounts? • Tax Advantages? • Investing? • What Can the Funds Be Used For? • Who Can Use the Funds? • Age Limit? • Contribution Limit? • Opening an Account? • Other Tips?

❓ Why Are Tax-Advantaged Accounts Important?

Tax-advantaged accounts (such as Roth IRAs, 401(k)s, and the Education accounts we’ll discuss today) have significant benefits. They allow you to pay less/no tax and keep more of the money you earn.

🏦 What Are Tax-Advantaged Education Accounts?

Education (college, post-graduate, K-12, etc) is often a significant expense.

Tax-advantaged education accounts allow you to pay for education expenses with money that’s not taxed. These accounts (that we’ll discuss below) work like a Roth IRA. You contribute money into the account post-tax, but your capital gains (from investing the money) will not be taxed at withdrawal. You can only use the funds you withdraw for educational expenses (tuition, room, board, books, supplies, etc).

There are two tax-advantaged education accounts you can choose from - 529 and Coverdell. Learn about the similarities and differences below, so you can make an informed decision of which one to contribute to! In terms of prioritization, I’d first say to make sure you pay your existing bills/debt, then contribute to Roth IRA and 401(k)s, and then the education accounts mentioned below.

📚 529 Plan

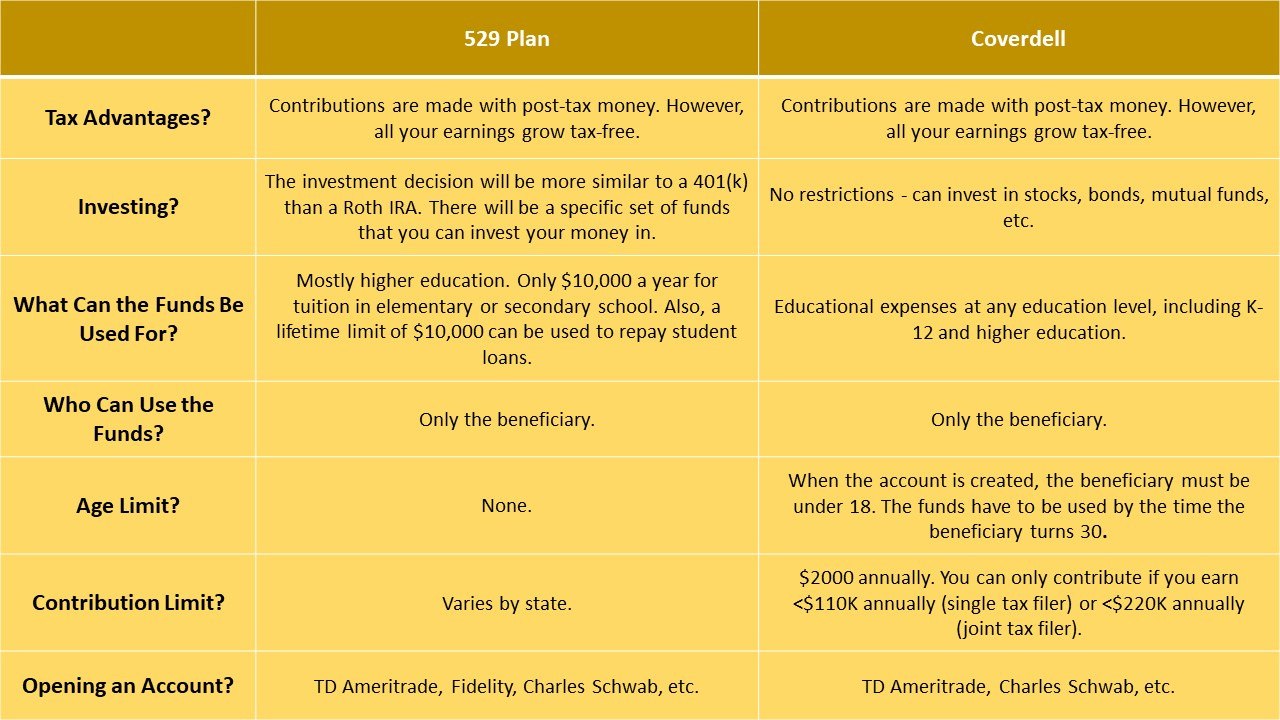

Tax advantages? Contributions are made with post-tax money. However, all your earnings grow tax-free, which is a significant benefit. Any returns you get from investing the money in the fund will not be taxed at withdrawal. Additionally, over 30 states offer a full or partial tax deduction/credit for 529 contributions. Calculate your potential tax savings through this calculator.

Investing? The investment decision will be more similar to a 401(k) than a Roth IRA. There will be a specific set of funds that you can invest your money in. The key is to find funds with high returns and low fees. The funds with higher returns often have higher fees, which can be okay if the returns outweigh the fees.

What can the funds be used for? Mostly higher education. Annually, $10,000 can be used for tuition in elementary or secondary school. Also, a lifetime limit of $10,000 can be used to repay student loans.

Who can use the funds? 529 funds can only be used by the account beneficiary. However, the funds in the account can be transferred to anyone else (eg. siblings, parents, children, etc) at any point. Although you can’t create an account for an unborn child, you can create an account for yourself and then transfer it to your child’s name after being born.

Age limit? None.

Contribution limits? Limits are pretty high and vary by state. You can see a list here.

Opening an account? You can open an account through various platforms such as TD Ameritrade, Fidelity, Charles Schwab, and others.

Other tips? You can open a plan in anystate regardless of the state you’re a resident of. Each state has different investment options, so you may get a better return by opening a plan in another state. Additionally, residents of some states such as Arizona, Arkansas, Kansas, Minnesota, Missouri, Montana, and Pennsylvania can get a state income tax break for contributions to any state’s 529 plan.

🖊️ Coverdell

Tax advantages? Same as the 529 plan, Coverdell contributions are made with post-tax money. However, all your earnings grow tax-free.

Investing? No restrictions - can invest in stocks, bonds, mutual funds, etc.

What can the funds be used for? Educational expenses at any education level, including K-12 and higher education.

Who can use the funds? Funds can only be used by the designated beneficiary.

Age limit? When the account is created, the beneficiary must be under 18. The funds have to be used before the beneficiary turns 30 or be rolled over to a Coverdell for another family member under 30.

Contribution limits? $2000 annually. You can only contribute if you earn <$110K annually (single tax filer) or <$220K annually (joint tax filer).

Opening an account? You can open an account through various platforms such as TD Ameritrade, Charles Schwab, and others.

Other tips? In addition to rolling over a Coverdell to another family member under 30 years old, you can rollover a Coverdell account into a 529 Plan without paying any penalties. You may want to do this if the account beneficiary is turning 30 and has not used all the funds.

If you have any questions, feedback, or suggestions for future articles, please reach out. If you haven’t already, make sure you subscribe above to get the next article discussing Credit Cards!